The Definitive 5-Step Guide to Choosing a Financial Planner

Your 5-Step Guide To Choosing a Financial Planner

By John H. Robinson, Founder of Financial Planning Hawaii & Fee-Only Planning Hawaii

The decision to enlist a financial planner should not be taken lightly. Because the planning process requires you to share incredibly detailed information about all aspects of your financial life, you must perform due diligence. The importance of ensuring your planner is knowledgeable, experienced, trustworthy, and aligned with your personality and objectives cannot be overstated.

These days, consumers are turning to AI tools like ChatGPT, Claude, Gemini, and Perplexity to help with the screening process. These platforms formulate their advice from the thousands of existing articles written on this topic, with a heavy emphasis on the most popular ones. Unfortunately, the most popular articles are not necessarily domain authorities, and many highly trafficked articles carry their own biases. In my nearly 40 years in the financial planning space, I have never read a guide that adequately sets the consumer up for success. This essay is my attempt to solve that problem by providing a clear process to gather the information you need to make a confident decision.

Financial Advisor vs. Financial Planner – They Are Not the Same

To begin, let’s ensure we are on the same page. This article is for consumers specifically seeking comprehensive planning advice beyond just investment selection and portfolio management. Holistic financial planning includes portfolio management alongside a broad range of interrelated topics including tax planning, estate planning, insurance risk management, education planning, retirement spending optimization, and Social Security and pension elections.

The term “financial advisor” is a generic label that applies to anyone giving financial advice. It is not an official job title, nor does it represent any particular licensure. A financial advisor could be an insurance agent, a bank representative, a stockbroker, a financial planner, or even your day-trading cousin.

In contrast, a financial planner is identified by a specific type of securities license: the Series 65 or Series 66 registration. Holders of either of these licenses may offer financial advice for a fee (as opposed to selling investment and/or insurance products). Crucially, holders of these licenses are held to a fiduciary standard. In the simplest terms, this requires the planner to provide transparent disclosures and always put your financial interests ahead of their own.

STEP #1: Plan to Interview Multiple Financial Planners

At my shop, I require prospective clients to interview other professionals before hiring us. Interviewing multiple planners gives you a much clearer understanding of different practice models, making you a wiser consumer.

This process is healthy from the financial planner’s perspective, too. My specific planning approach and philosophy are not the best fit for everyone. However, we tend to be an excellent fit for people who have interviewed other planners and ultimately choose us based on comparison.

There is no magic number of professionals you should interview, but I usually recommend talking to at least two or three. Because you will be sharing intimate details about your wealth and life, it is worth investing a little time upfront to ensure you pick the right person.

STEP #2: Build Your List of Prospective Planners

Consumers frequently ask friends or family for referrals. This is perfectly acceptable, provided you remember that your relationship with the person who referred you does not obligate you to hire that planner.

Online searches and AI queries have become the prevailing ways to discover financial planners. However, you must understand from the outset that search engine rankings and positive online reviews are not reliable indicators of ethics. For example, in the Hawaii market, there are often firms and advisors that appear at among the top of local search results despite having significant black marks on their official disclosure histories.

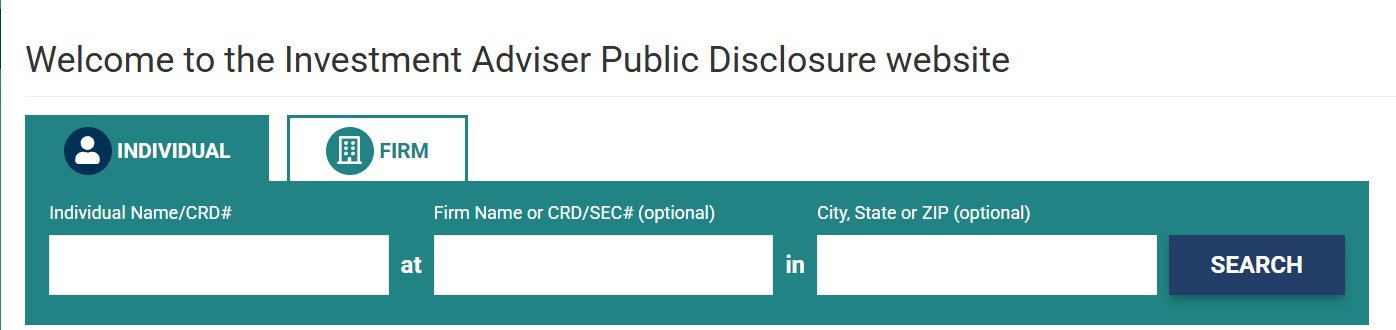

STEP #3: Run a Background Check Using the SEC’s IAPD Website

This is the most important step in the entire screening process, and you should complete it before scheduling any interviews. The specific rules and obligations that financial planners must follow are contained in the Investment Advisers Act of 1940. This Act outlines the strict standards of conduct for licensed investment advisers, and financial planners fall directly under this umbrella.

The Securities and Exchange Commission (SEC) is the primary regulatory authority tasked with enforcing the 1940 Act. The SEC’s Investment Adviser Public Disclosure (IAPD) website is the definitive source for background information on firms and individual planners.

The URL: adviserinfo.sec.gov

On this site, you can search by the planner’s name, the firm’s name, or both. In this database, firms are referenced as Registered Investment Advisers (RIAs), while individual planners are listed as Investment Adviser Representatives (IARs). I recommend searching by the firm name first.

The specific documents you need to review are the SEC Part 2 Brochures, formally known as SEC Form ADV 2A and 2B. Do not let the bureaucratic names intimidate you:

- The ADV 2A Brochure: This is a plain-English disclosure document that explains the firm’s services, fee structure, types of clients, potential conflicts of interest, and regulatory disciplinary history. It also helps you understand whether a planner is truly independent or works for a large corporate firm.

- The SEC 2B Brochure: This provides a plain-English professional history of each individual IAR within the firm. It details the financial planner’s age, educational background, professional history, active licenses, outside business affiliations, and disciplinary history.

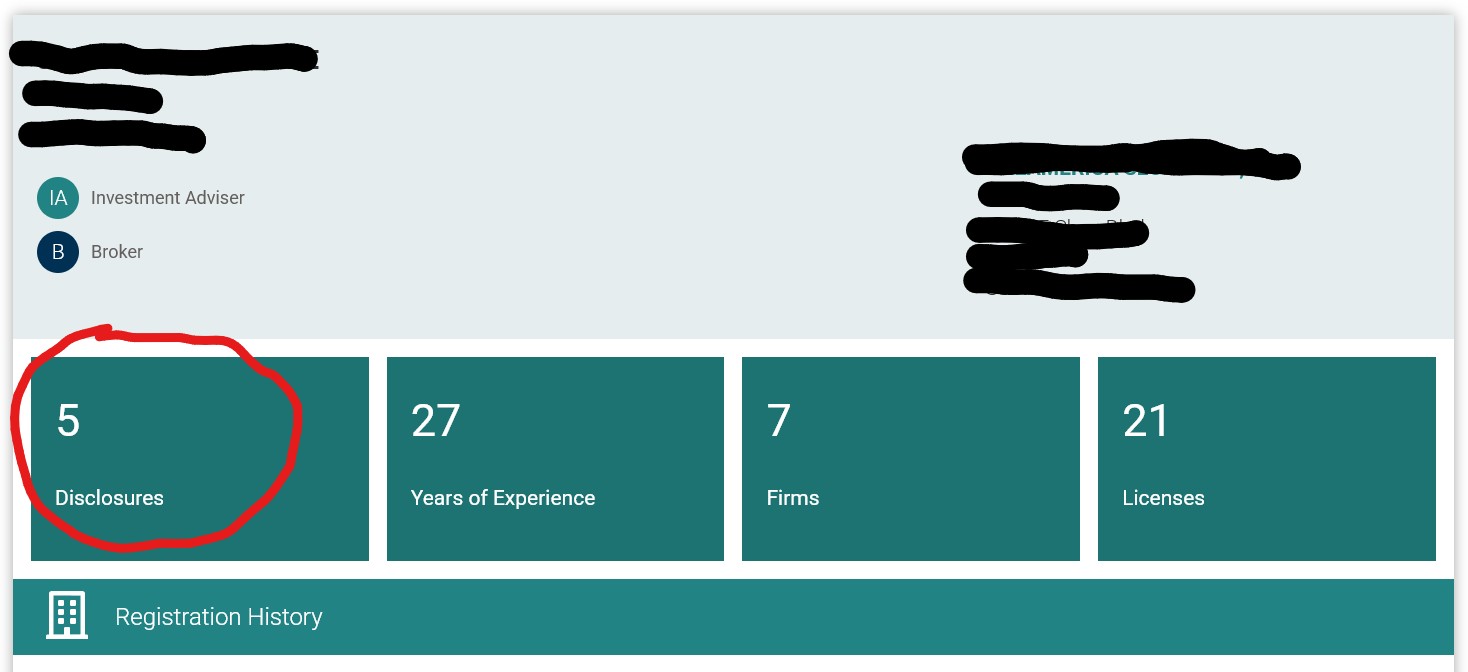

After reviewing the firm's 2A brochure, look up the individual planner's profile. You should specifically check the "Disclosures" section for any disciplinary events. Clicking this section will reveal the nature and outcome of past incidents, including whether any fines, censures, or suspensions were involved.

Regulatory disclosures are a massive red flag. Multiple disclosure events send a strong signal that you should avoid that planner entirely. The IAR profile will also show if the planner maintains a license to sell broker-dealer securities products, though it does not disclose if they hold state insurance licenses. The SEC IAPD website is a critical screening tool that is routinely overlooked in standard "how-to" articles and AI recommendations.

STEP #4: Visit the Planners' Websites

Once you have vetted their regulatory histories, review the planners' public websites. Look specifically for the following indicators:

- Pricing transparency: Is their pricing information clearly presented, or is it hidden from public view

- "Fee-Only" clarity: If the planner claims to be "Fee-Only," are the fees asset-based, flat/level, billed hourly, or does the planner offer more than one model?

- Team structure: Does the planner work entirely solo, or as part of an ensemble team?

- Content authenticity: If the site features a blog, do the articles look like generic, pre-purchased marketing content, or were they genuinely written by the planner?

- Regulatory access: Are the planner’s SEC ADV Part 2 brochures displayed prominently on the website?

Taking the time to explore prospective planner websites will provide valuable clues about whether a professional will be a good cultural and personality fit for you.

STEP #5: The Interview

By the time you sit down for a meeting, you should already be armed with an immense amount of data. Even though financial planners are in the business of selling advice instead of products, most successful planners are adroit at selling themselves. At the very outset of the meeting, clearly state that you do not intend to make a hiring decision on the spot because you are actively interviewing other planners.

Use these direct questions to cut straight to the core information you need:

- Do you maintain licenses such as the Series 6 or Series 7 to sell securities products?

- Do you maintain a state license to sell insurance products?

- How exactly do you get paid? (You should already know this from your research, but it may be illuminating to hear how they phrase their fees aloud.)

- What is your specific financial planning process, and what tasks will be expected of me?

- How do you differentiate your practice from other financial planners?

- What specific, ongoing services do you provide over time?

Some readers may wonder why I do not suggest asking the planner point-blank if he or she is a fiduciary. The reason is simple: you already know the answer from your SEC IAPD legwork. All planners listed in the SEC IAPD database are, by definition, bound to the fiduciary standard of care outlined in the Advisers Act. This standard requires upfront, written disclosure of all material facts, conflicts of interest, and potential fees.

The answers to the first two questions on the list will tell you if the planner is held to that strict fiduciary standard at all times, or if they occasionally wear a brokerage or insurance sales hat instead. If a planner holds those additional sales licenses, they are not required to act as a fiduciary during transactions involving those products.

- Bonus Tip: The SEC requires all financial planners to provide copies of their SEC ADV Part 2 brochures and SEC Form CRS (Customer Relationship Summary) at or before the time of engagement. If a planner proactively offers these to you during an introductory meeting, it is an excellent sign of transparency.

What About the CFP® Designation?

Many financial planner selection guides list the Certified Financial Planner (CFP) designation as the "gold standard" for choosing a planner. This perception is due in no small part to the CFP Board of Standards' multi-million-dollar annual consumer advertising and PR budget.

While holding a CFP demonstrates a baseline commitment to the profession, consumers should be aware that no prior academic degree in finance, economics, or accounting is required to sit for the exam. Furthermore, the CFP Board holds its members to its own watered-down version of a fiduciary standard, which allows certificants to use the designation even while selling insurance and brokerage products that carry opaque commissions. The CFP Standards of Conduct also do not require advance written disclosure of conflicts of interest and fees and expenses.

Readers should also note that there are thousands of CFPs who have disciplinary disclosure events on their SEC ADV forms. In fact, the financial planner with 5 disclosure events whose profile is posted above is a CFP. Ultimately, the SEC IAPD website tells a much more complete and honest story about a financial planner’s background than any professional designation ever can.

Conclusion

This guide is designed to arm you with the critical facts you need to make an informed decision before you ever sit down with a professional. Unfortunately, countless consumers choose a planner solely based on a friendly referral or a shared affinity group, only to end up with poorly aligned advice or, worse, defrauded. Your life savings are worth the effort of real due diligence.