Trump Account vs. 529 Plans - Which is better?... It Depends

By J.R. Robinson, Financial Planner (May 2026)

Now that the IRS has issued formal guidance on many, though not all, of the rules for Trump accounts, the financial planning community is working to determine how this new instrument fits into the existing ecosystem. Of particular interest is how Trump accounts, also referred to as “530 A” accounts and “American Dream accounts,” compare to 529 plans, more formally known as qualified tuition programs. This article explains the circumstances that may favor one over the other.

Trump Accounts and 529 Plans: The Basics

The Trump account concept traces back to Brad Gerstner, founder and CEO of Altimeter Capital, who proposed government funded “Invest America” accounts for children at birth that could only be accessed in adulthood to help pay for education or entrepreneurship as a potential low-cost way to address multigenerational poverty. The Trump account adopts some of these ideas and is being introduced as a pilot program from 2025 through 2028. During this period, the federal government pledges to contribute $1,000 per child born during the pilot years.

In addition to the seed contribution, total additional contributions of up to $5,000 per year can be made until the child reaches age 18. Trump accounts may also be established for older children up to age 18, but these accounts do not receive the $1,000 dollar government funding. Contributions may come from family members, other individuals, and corporations. All funds must be invested in ultra low-cost stock market index funds.

No distributions are permitted before the calendar year in which the beneficiary turns 18. Beginning in that year, the account may be used for certain qualifying expenses, including education, first time home ownership, or entrepreneurship. Distributions are taxable on a pro rata basis relative to the total contribution amount, but they avoid a 10% penalty if used for qualified expenses. Trump account assets may also be left to continue to grow tax- deferred for retirement or converted to a Roth IRA, where they can grow tax free for retirement.

By contrast, 529 plans were created under the Small Business Job Protection Act of 1996, which added Section 529 to the Internal Revenue Code to promote saving for education expenses. The law allowed individual states to sponsor plans that enable consumers to make after-tax contributions to a menu of mutual funds. Earnings may be distributed tax- free if used for qualifying higher education expenses.

Originally, qualified expenses were limited to post-secondary tuition. Over the last three decades, the definition has been expanded to include K-12 private tuition expenses (within limits), trade schools, and certain professional certifications. Although individual 529 plans have total contribution limits, typically around $300,000, there is effectively no overall cap per child. Parents, grandparents, or others can establish multiple 529 plans for the same beneficiary.

529 plan owners also have significant flexibility to change the beneficiary. They may move the account from one child to another, apply unused funds to yet unborn grandchildren, or even name themselves as beneficiaries. Withdrawals for non-qualified purposes are subject to ordinary income tax and a 10 percent IRS penalty applied to the earnings portion of the distribution.

In 2023, the SECURE Act 2.0 created the opportunity to roll remaining 529 balances of up to $35,000 to the beneficiary’s Roth IRA tax- and penalty-free, subject to the annual Roth IRA contribution limit. To qualify, the 529 account must have been in place for at least 15 years and the money must have been invested for at least the previous five years. Other restrictions may apply as well.

Which Is Better for Education Funding?

The answer is not as clear as it might seem at first glance. Trump accounts offer a $1,000 government seed for eligible newborns, but 529 plans allow much larger dollar amounts to be contributed from birth onward into low expense funds that can later be distributed tax-free for qualifying education expenses, including K-12 private school tuition. That combination makes 529 plans appear to be the clear winner for many families whose primary focus is education funding.

The disparity may be even greater for moderate to high earning parents because of the application of the IRS kiddie tax rules to Trump account distributions. Under these rules, taxable unearned income for a dependent child above a threshold amount is taxed at the parents’ top marginal tax rate. There does not appear to be any exception for Trump account withdrawals used for qualifying education expenses in the current IRS guidance, which further reduces their relative advantage for education.

However, in practice, Trump accounts may be an excellent choice for lower income and impoverished families who are unlikely to be introduced to or able to contribute meaningfully to 529 plans. Public awareness and the $1,000 incentive for children born between January 1, 2025 and December 31, 2028 should go a long way toward providing at least a modest financial boost at adulthood. If family income remains low through age 18 or if the beneficiary waits until age 24 to convert and has little or no taxable income, there may be little or no tax owed on a Roth conversion.

While families starting from poverty are unlikely to make substantial additional contributions to either Trump accounts or 529 plans, Trump accounts offer a unique feature that can help. Employers can contribute up to $2,500 per employee, not per employee’s child. The contribution is deductible for the company, not subject to payroll tax, and not taxable as income to the employee. This appealing feature does not exist within 529 plans.

Which Is Better for Retirement Savings?

Financial planners and sophisticated consumers have long wished for a tool that would allow retirement saving to begin at birth. The stumbling block has always been the earned income requirement for traditional and Roth IRAs. Although some children do earn income from social media ventures or name, image, and likeness deals, most young children do not meet the earnings requirement.

The Trump account offers a pathway around this barrier. Beginning at age 18, Trump account beneficiaries may roll their accounts into traditional IRAs, with the important caveat that they must maintain careful records of after-tax contributions to avoid double taxation. Alternatively, they may convert Trump account balances to Roth IRAs. Beneficiaries should understand that any income tax due on a Roth conversion should ideally be paid from personal savings or gifts, not from the Trump account itself. While it is permitted to have tax withheld from the conversion amount, the IRS imposes a 10 percent penalty on any amount distributed to pay the tax. Conversions before age 24 should also take into account the potential impact of kiddie tax rules.

An alternative approach that has received almost no attention in the media or planning community is to roll the Trump account into a traditional IRA, then process partial Roth conversions over time to optimize and minimize tax liability. This staged conversion strategy could be particularly powerful during years when the beneficiary has low taxable income.

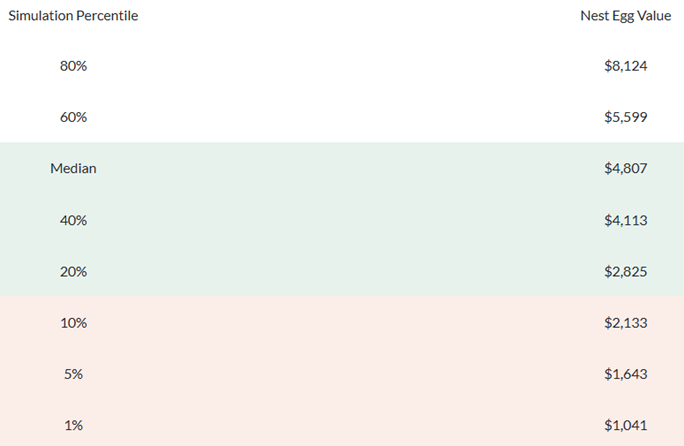

Projected Value of a $1,000 Trump Account after 17 Years Assuming No Future Contributions and a 100% Allocation to an S&P 500 Index Fund with a .05% expense ratio:

Source: Nest Egg Guru College Savings App

Projected Value of a Trump Account after 17 Years Assuming Maximum $5,000 Annual Contributions and a 100% Allocation to an S&P 500 Index Fund with a .05% expense ratio:

Source: Nest Egg Guru College Savings App

For 529 plans, the retirement opportunity is much more limited. As noted earlier, beneficiaries may convert up to a total of $35,000 through direct rollovers to Roth IRAs. There is no earned income requirement for these rollovers, but making a rollover contribution from a 529 plan precludes the beneficiary from making an additional IRA or Roth contribution in the same year. In that sense, 529 plans offer a useful safety valve for leftover funds but not a full-fledged early retirement vehicle.

Which Is Better for Uses Beyond College and Retirement?

Trump accounts have a couple of unique qualified distribution alternatives that do not exist for 529 plans. Specifically, they allow qualified distributions for a first-time home purchase or for funding a new business. These withdrawals are exempt from the 10% penalty, although they are still taxable as income on a pro rata basis relative to after-tax contributions and earnings.

By contrast, 529 plans offer an advantage for families who anticipate private K-12 schooling. Owners may pay up to $20,000 per beneficiary per year to help cover private K-12 tuition. These distributions are exempt from federal income tax, although they may be taxable at the state level. Trump accounts cannot be tapped before the year in which the beneficiary turns 18, so they are not available for K-12 tuition.

529 plans also provide much more flexibility to change beneficiaries and support multigenerational planning. Unused balances from accounts established for the owner’s children can be redirected to their eventual grandchildren. As mentioned earlier, 529 plan owners can establish multiple plans for children. By contrast, only one Trump account may be established for each child, which significantly limits flexibility.

Trump Accounts vs 529 Plans: The Verdict

For education funding, this analysis concludes that all families with children born during the pilot period should take advantage of the government’s $1,000 gift by establishing a Trump account. Families with modest to higher income levels may be better served by favoring 529 plans for subsequent contributions while still taking full advantage of any employer benefits that include Trump account funding. For beneficiaries from lower income households, Trump accounts may be a sound choice for additional contributions toward education planning. The new rules may even encourage workers to seek out employers that offer Trump account contributions as an employee benefit.

For retirement funding, the long standing mantra in the financial planning community is to invest as much as you can for as long as you can. For families with the means or opportunity to make ongoing contributions to a Trump account, either on their own or with employer assistance, it is realistically possible, depending on the contribution level, to accumulate $200,000 or more by age 18. Rolling that balance to a traditional IRA or converting it to a Roth IRA would give young adults an enormous head start on retirement security. This kind of early savings may also make it more palatable for them to pursue lower paying career paths that align more closely with their passions, rather than feeling compelled to prioritize jobs that offer greater financial security. If the primary objective from the outset is to provide retirement security for the child, the Trump account appears to be the clear winner relative to 529 plans.

When it comes to other uses beyond education and retirement, the verdict is essentially a draw. Trump accounts are better for families that want the option to use accumulated investments to start a business or buy a home. 529 plans are better for families that may use the accounts for K-12 tuition or that value the flexibility to establish multiple plans, support multigenerational education funding, or change the beneficiary to another child or even to themselves.

Conclusion

As a financial planner, I view the Trump account as an intriguing new planning tool with many potential applications. For families with children born during the pilot program, there is little reason not to establish a Trump account. Consumers should also ask employers whether they plan to include Trump account funding in their benefits programs.

Beyond those considerations, I believe families who prioritize saving specifically for education expenses are best served by adopting 529 plans as their primary education vehicle. Families who wish to retain flexibility over how funds may ultimately be used, including post-secondary education, home purchase, business start-up, and retirement, may do well to establish and continue to fund a Trump account. They should keep in mind that after the year in which the child turns 18, they will have the option to convert to a Roth IRA or roll the Trump account to an IRA and later execute partial Roth conversions.

It is also important to remember that the decision to fund Trump accounts and 529 plans does not need to be an either/or choice. I envision instances where consumers establish a Trump account at birth to support future home purchase, business start-up, and retirement planning while also setting up a 529 plan for education funding.

Finally, it is worth revisiting the societal benefit that underlies Brad Gerstner’s initial premise for Trump styled accounts. Although a single $1,000 contribution will likely grow to only about $5,000 dollars over 18 years, additional contributions from families and employers can give these accounts a meaningful positive impact on the beneficiary’s future life choices. For some children, the Trump account may provide a direct pathway out of poverty. If earmarked for retirement, it has the potential to go a long way toward securing long term financial stability, which in turn may allow beneficiaries to pursue careers that reflect their ideals and passions.

At this time, the $1,000 incentive for newborns is only available as a four year pilot program. Anyone with children under age 18 may establish a Trump account beginning July 4, 2026 by submitting IRS Form 4547. The entire enrollment process is outlined on TrumpAccounts.gov.

John H. Robinson is the owner/founder of Financial Planning Hawaii and Fee-Only Planning Hawaii.

Supporting Documents

IRS Issues Guidance on New Trump Accounts for Children (Human Resources & Payroll)

- IRS Issues Initial Guidance Regarding Trump Accounts, Including Employer Contributions Pursuant to a Trump Account Contribution Program (Skadden Arps Law Firm)

- The Hack That Turns Trump Accounts Into Multimillion-Dollar Tax-Free Nest Eggs (Wall Street Journal)