Tax Rate Arbitrage

By John H. Robinson, Financial Planner (June 2026)

A large traditional IRA was once among the most valuable assets a family could pass on to the next generation. It represented decades of disciplined saving and tax-deferred growth. However, an under-the-radar rule change enacted through the SECURE Act of 2019 created a significant tax challenge for many IRA owners and fundamentally altered the guidance financial planners and tax professionals had long provided regarding pre-tax retirement accounts.

For decades, conventional wisdom encouraged workers to maximize contributions to pre-tax retirement accounts such as IRAs, 401(k)s, and 403(b)s during their highest-earning years. The expectation was that distributions would be taken later in retirement when income and tax rates were generally lower. Any remaining balance could then be passed to children, who could stretch distributions over their own life expectancies while continuing to benefit from decades of tax-deferred growth.

The SECURE Act largely eliminated that strategy for most non-spouse beneficiaries. Adult children who inherit a traditional IRA must now generally distribute the entire account within ten years of the original owner’s death. Unfortunately, many beneficiaries inherit these accounts during their 40s and 50s, which are often their peak earning years. The inherited IRA distributions are layered on top of already substantial income, potentially pushing beneficiaries into higher marginal tax brackets.

The result is a rapid acceleration of taxable income and a meaningful reduction in after-tax wealth. This is the phenomenon that leading IRA expert Ed Slott, CPA, refers to as the “IRA Tax Bomb.” Without thoughtful planning, it often detonates at precisely the wrong time.

From a Legacy to a Tax Burden

Prior to the SECURE Act, a child who inherited an IRA could generally stretch required distributions over his or her life expectancy. Because required minimum distributions were often relatively small, the bulk of the account could continue growing tax deferred for decades.

Today, most non-spouse beneficiaries must fully distribute inherited IRA assets within ten years of the original owner’s death. Compressing distributions into a ten-year window instead of a 30- to 40-year distribution period dramatically accelerates taxation. The problem becomes even more pronounced because many beneficiaries inherit these assets during their highest-earning years.

As a result, inherited IRA distributions are often taxed at substantially higher marginal rates than they would have been if distributed gradually over a beneficiary’s lifetime. The combined effect can significantly reduce the after-tax value of what was intended to be a meaningful family legacy.

Tax Rate Arbitrage

Tax bracket arbitrage offers a practical strategy for addressing this problem. The concept is simple. If taxes are unavoidable, the objective becomes controlling when they are paid and at what tax rate.

By recognizing income earlier at lower tax rates and spreading future taxable income among multiple taxpayers, families may be able to reduce the overall tax burden imposed on retirement assets.

In some cases, the goal is not minimizing this year’s tax bill. The goal is minimizing the family’s cumulative lifetime tax liability across two generations.

Two primary strategies can help accomplish this objective. The first is the use of partial Roth conversions during the original owner’s lifetime. The second is thoughtful beneficiary design that may, in some circumstances, include both children and grandchildren.

Roth Conversion Planning

A Roth conversion transfers a portion of a traditional IRA into a Roth IRA and creates taxable income in the year of conversion. While voluntarily accelerating taxable income may seem counterintuitive, it can be highly effective when implemented strategically.

For some households, this may mean gradually processing partial Roth conversions over many years to fill lower marginal tax brackets. For households with particularly large IRA balances, especially those whose future required minimum distributions and projected inherited IRA distributions could expose both themselves and their heirs to substantially higher tax rates, it may be advantageous to target a higher effective tax rate today rather than focusing exclusively on filling lower marginal brackets.

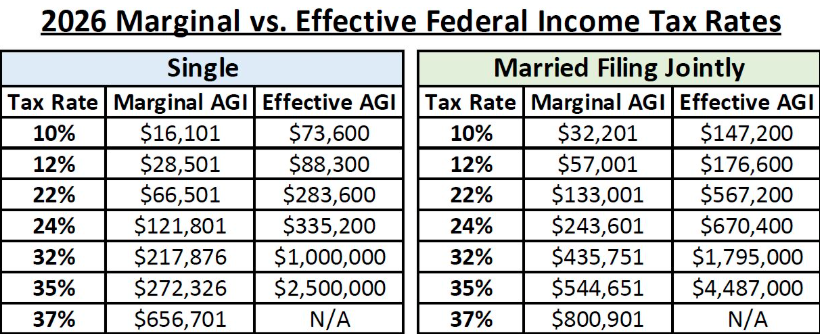

Nerd Wallet Effective Federal Income Tax Calculator

For example, a married couple filing jointly in 2026 with $300,000 gross income may consider converting as much as $135,000 of pre-tax IRA money utilize the 24% marginal tax bracket. With AGI of $435,000 the 2026 effective federal income tax rate might be roughly 20.32%, (assuming the standard deduction)

By contrast, if this same household has substantial retirement assets and potentially large future tax liabilities for both themselves and their heirs,they may choose to target an effective tax rate closer to 24%. Per the table above, an effective tax rate of 24%, is produced with an AGE of just over $670,00. Instead, of converting $135,000, they would now convert as muchas $370,00.

The appropriate strategy depends on individual circumstances, current tax rates, projected future income, estate planning objectives, and the anticipated tax situations of beneficiaries.

The benefits of Roth conversion planning may include:

• Lower future required minimum distributions (RMDs)

• Increased tax-free assets available for retirement spending

• Elimination of RMDs from Roth IRAs during the owner’s lifetime

• A more tax-efficient legacy for heirs

Tax Planning Considerations for Roth Conversions

Although Roth conversions can be powerful planning tools, they involve numerous tax considerations that should be discussed with a CPA or qualified tax advisor before implementation.

Individuals under age 59½ should ensure they have sufficient liquid assets outside the IRA to pay the taxes generated by the conversion. If taxes are withheld from the converted amount, the withheld funds may be treated as a premature distribution and could be subject to a 10% IRS penalty.

Individuals over age 59½ have greater flexibility. While many advisors recommend paying conversion taxes from after-tax savings so that the entire converted amount can continue growing within the Roth IRA, withholding taxes from the conversion itself remains a valid option when outside funds are unavailable.

Conversions may also provide additional benefits for residents of states with significant estate taxes, including Hawaii, Massachusetts, Rhode Island, Connecticut, New York, and Oregon. Paying taxes during life reduces the value of the taxable estate, potentially lowering future estate tax exposure.

Individuals age 63 and older should also consider the impact of conversions on Medicare premiums. Medicare Part B and Part D premiums are subject to Income-Related Monthly Adjustment Amount (IRMAA) surcharges when income exceeds specified thresholds. Because IRMAA calculations are based on income from two years earlier, a large Roth conversion can create higher Medicare premiums in future years.

Taxpayers with substantial investment income (including rental income, dividends, capital gains, interest income, etc) should also be mindful of the 3.8% Net Investment Income Tax surcharge (NIIT). While Roth conversions themselves are not subject to the tax, higher adjusted gross income may cause more investment income to become exposed to the surcharge.

Social Security claiming decisions should likewise be coordinated with conversion planning. In some situations, delaying Social Security benefits beyond Full Retirement Age may create additional low-income years that are ideal for Roth conversions. Individuals who have already claimed benefits may wish to evaluate whether temporarily suspending benefits during significant conversion years is appropriate.

Required minimum distributions also play a critical role in Roth conversion planning. Since RMDs increase taxable income, many retirees benefit from maximizing Roth conversions during the years before RMDs begin. Equally important, taxpayers must fully satisfy their annual RMD before processing a Roth conversion. Under IRS rules, the first dollars distributed from an IRA each year are deemed to satisfy the RMD, and RMD amounts are not eligible for conversion. Failure to follow this rule can create excess contribution penalty issues within the Roth IRA.

Ed Slott: What Retirees Need to Know About Required Minimum Distributions(Ed Slott)

Beneficiary Design Considerations

For individuals with children and adult grandchildren, beneficiary design may offer additional opportunities for tax-rate arbitrage.

One strategy worth considering is naming one or more adult grandchildren as beneficiaries alongside adult children. The rationale is straightforward. Young adult grandchildren are often in much lower tax brackets than their parents. As a result, inherited IRA distributions received by grandchildren may be taxed at significantly lower rates.

From a purely tax-planning perspective, dividing pre-tax retirement assets among a larger number of independent taxpayers may reduce the family’s aggregate tax liability.

This strategy may be particularly attractive for grandparents with a single child and multiple adult grandchildren. There is also no requirement that beneficiary allocations be equal. In some cases, directing a portion of retirement assets to grandchildren may reduce future financial support obligations for parents by helping fund major expenses such as graduate school, weddings, or first-time home purchases.

Of course, tax planning is only one consideration. Family dynamics can quickly complicate beneficiary decisions. What appears optimal from a tax perspective may create unintended emotional or relational consequences among family members.

Readers should also recognize that this strategy generally works best when beneficiaries are independent adults. For younger beneficiaries, the Kiddie Tax rules may apply which could cause distributions received by dependent grandchildren may be taxed at their parents’ higher marginal tax rates, reducing the anticipated tax benefit.

For beneficiaries who are approaching independence, careful distribution planning may help minimize exposure to the Kiddie Tax while preserving the long-term value of inherited retirement assets.

Inheriting Grandma’s IRA (Veritage Law Group)

Don’t Leave Grandchildren with a Tax Bill (Sims & Campbell Estates & Trusts)

Summary

The SECURE Act fundamentally changed the economics of inherited traditional IRAs. What was once an exceptionally effective multigenerational wealth-transfer vehicle can now create substantial tax burdens for beneficiaries during their peak earning years.

Fortunately, families are not powerless. Strategic Roth conversions, careful management of tax brackets, and thoughtful beneficiary design can significantly reduce the long-term tax cost associated with retirement assets.

The key is proactive planning. By addressing these issues years before they become a problem, IRA owners can improve their own tax efficiency, reduce future required minimum distributions, and leave a more valuable after-tax legacy to the next generation.

While my purpose in crafting this piece is to raise awareness of opportunities to reduce/optimize tax on large IRAs in a post- SECURE Act world, it should also be clear that there is enough tax complexity that your CPA or tax advisor should be included in all such planning discussions.

John H. Robinson is the founder of Financial Planning Hawaii and Fee-Only Planning Hawaii